Tsuburaya (“TFH” or the company) engages in distributions of Pachinko/Pachislot machines. It was created after Fields Corporation, a Pachinko/Pachislot machine manufacturer, acquired 51% of Tsuburaya Productions, a content creator in 4/20.

TFH conducts its operations through three entities.

1) Tsuburaya Productions plans and produces movies and television programs such as Ultraman. It also earns licensing revenues.

2) Digital Frontier plans and produces computer graphics.

3) Fields operates pachinko/pachislot segments.

Note:

1) Some view Pachinkos as “social evils” since playing on pachinko machines can be addicting. If you would like to avoid investing in gaming stocks, please skip this report.

2) Shared Research offers a detailed description of TFH’s corporate history. Their report is available in English for free.

How Do Pachinko Machines Work?

- Pachinko is played on a pinball-like vertical board.

- The game’s objective is to shoot small metal balls into the board and then have them bounce off pins and other obstacles to landing in certain pockets.

- If the ball falls into the winning pockets, the player will receive more balls, which can be exchanged for prizes.

Players have a limited amount of control over the flow of the game by utilizing levers to inject balls into the circuit or to manipulate traps inside the machine. One small silver ball can be bought from somewhere between 1 to 20 Japanese yen, depending on the machine. Most pachinko players spend over JPY 10,000 (about $100) per parlor visit, making the pachinko business lucrative.

Investment thesis in one paragraph:

Tsuburaya is an independent pachinko machine distributor in an industry which is finally on an early stage of recovery from a regulation imposed funk and population decline. Its right to distribute “Ultraman franchise” contents add to its profit growth.

This investment thesis is further analyzed in the following section.

1.Investment thesis

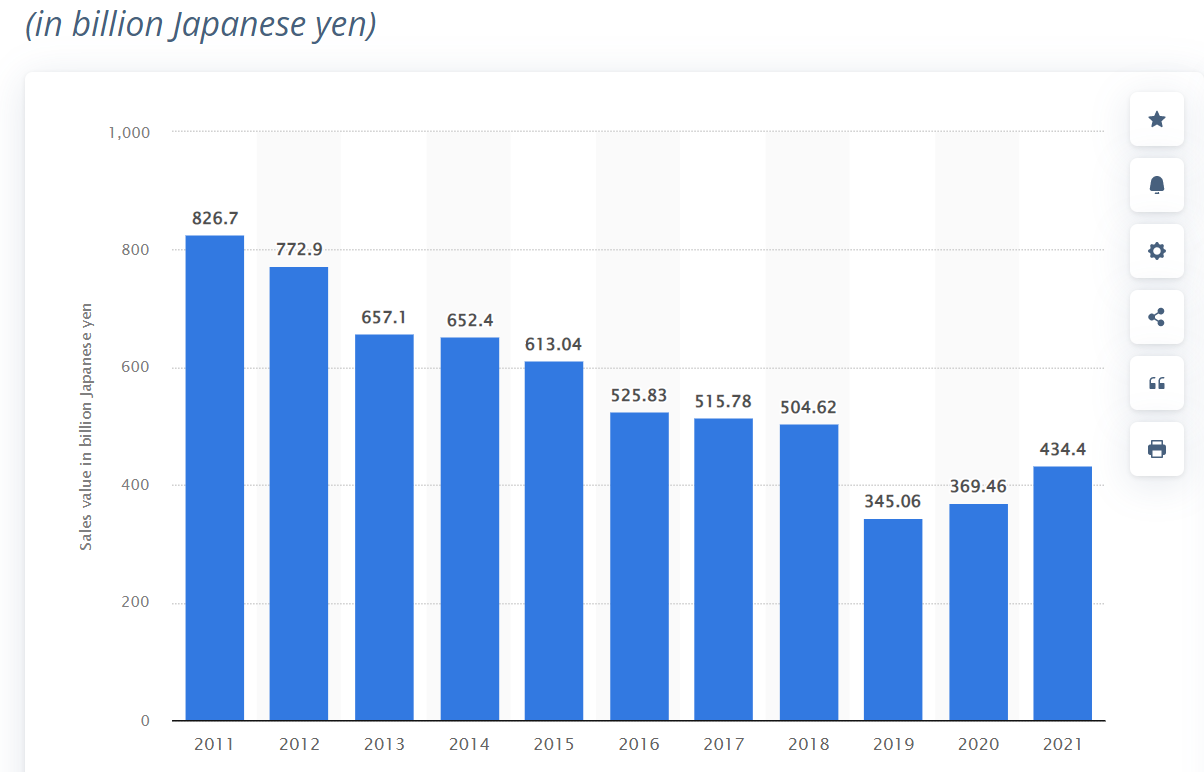

1) The pachinko industry is finally recovering from “Regulatory Overhang”?

Regulations on pachinko and pachislot machines are revised every 10 years, with the previous regulations reviewed regarding their impact on consumers. New regulations tend to lessen gambling elements, with which machine makers cope by developing machines with gambling features toned down. Instead, the industry is working hard to improve “Entertainment/Leisure amusement aspects” of pachinko/pachislot.

The company believes that a recent move away from dependency on high gambling nature machines toward healthier and more entertainment-oriented machines should resume growth for the pachinko industry in the near future.

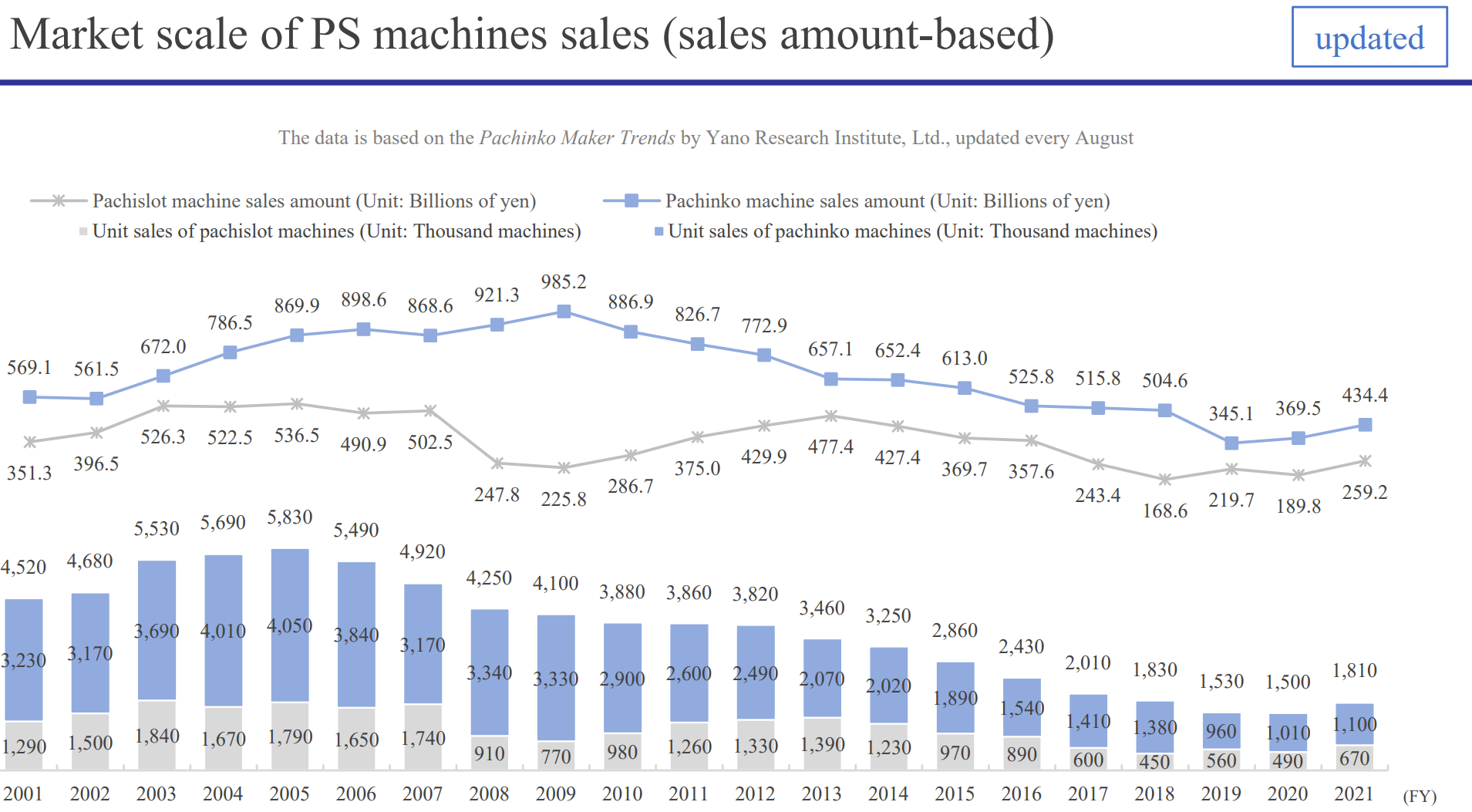

The pachinko machine sales recovery in the below graph from Statista may point to possibility that the above hypothesis is playing out.

(Source: Pachinko machines market sales value in Japan FY 2011-2021, By Statista as of 10/20/22)

Against this industry backdrop, TFH aims to partner with more pachinko and pachislot manufacturers and acquire rights to promising entertainment content, thereby selling more machines sold per title. In FY 3/23, the company plans to release 7 pachinko titles (6 in FY03/22) and 8 pachislot titles (7 in FY03/22). In the future, the company aims to release 12 pachinko and 12 pachislot titles a year by increasing the number of partner manufacturers.

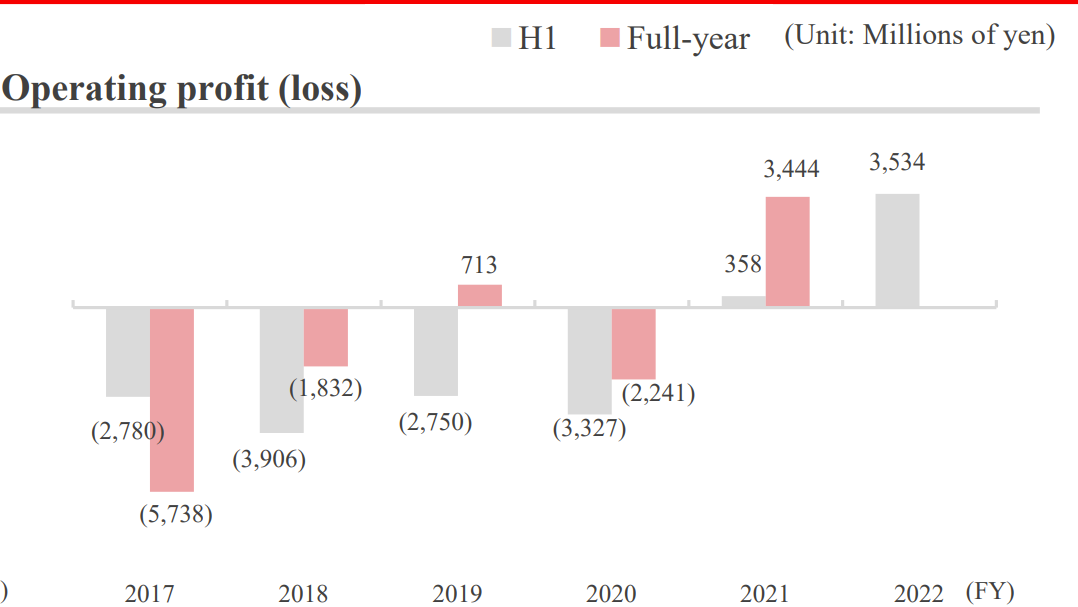

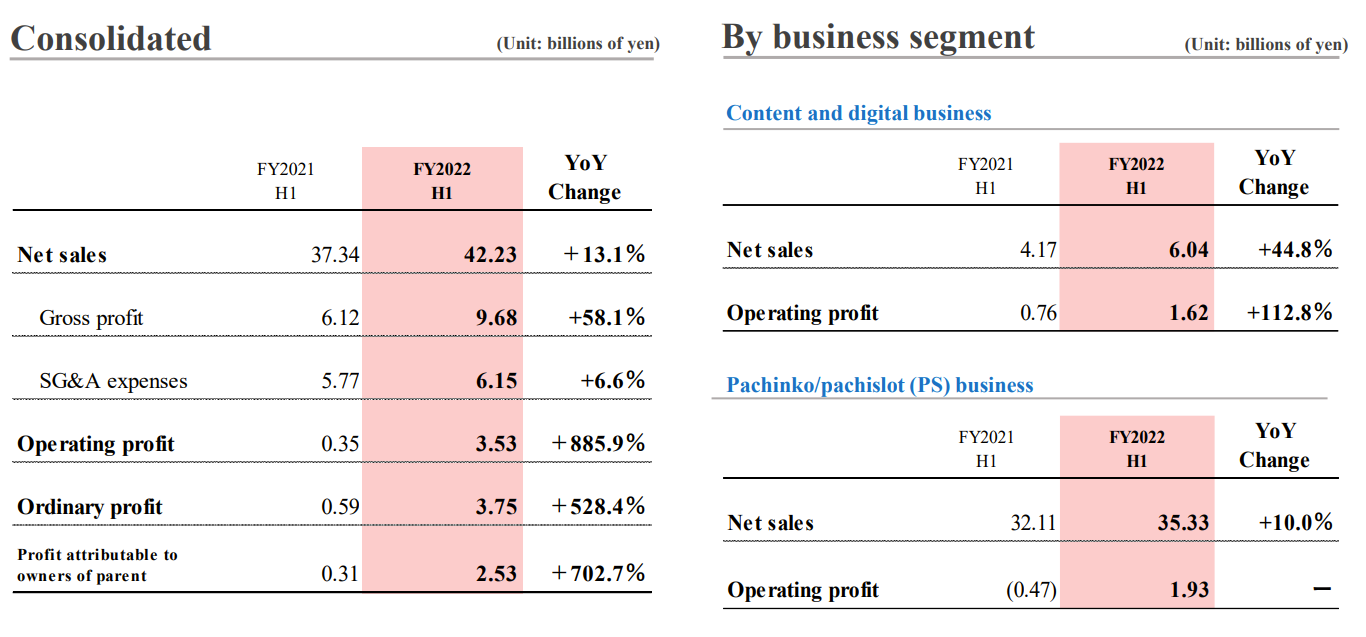

The below chart highlights operating profit recovery TFH witnessed over the last few years. In fact, during the first 6 months of 2022, operating profits had already exceeded a full year operating profits for FYE 3/21.

(Source: Fact Book 1 Q2 2022)

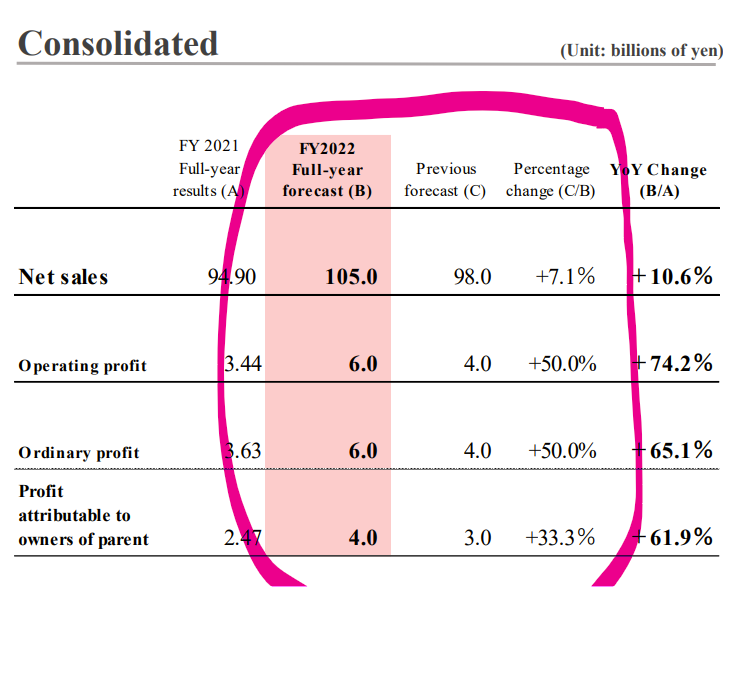

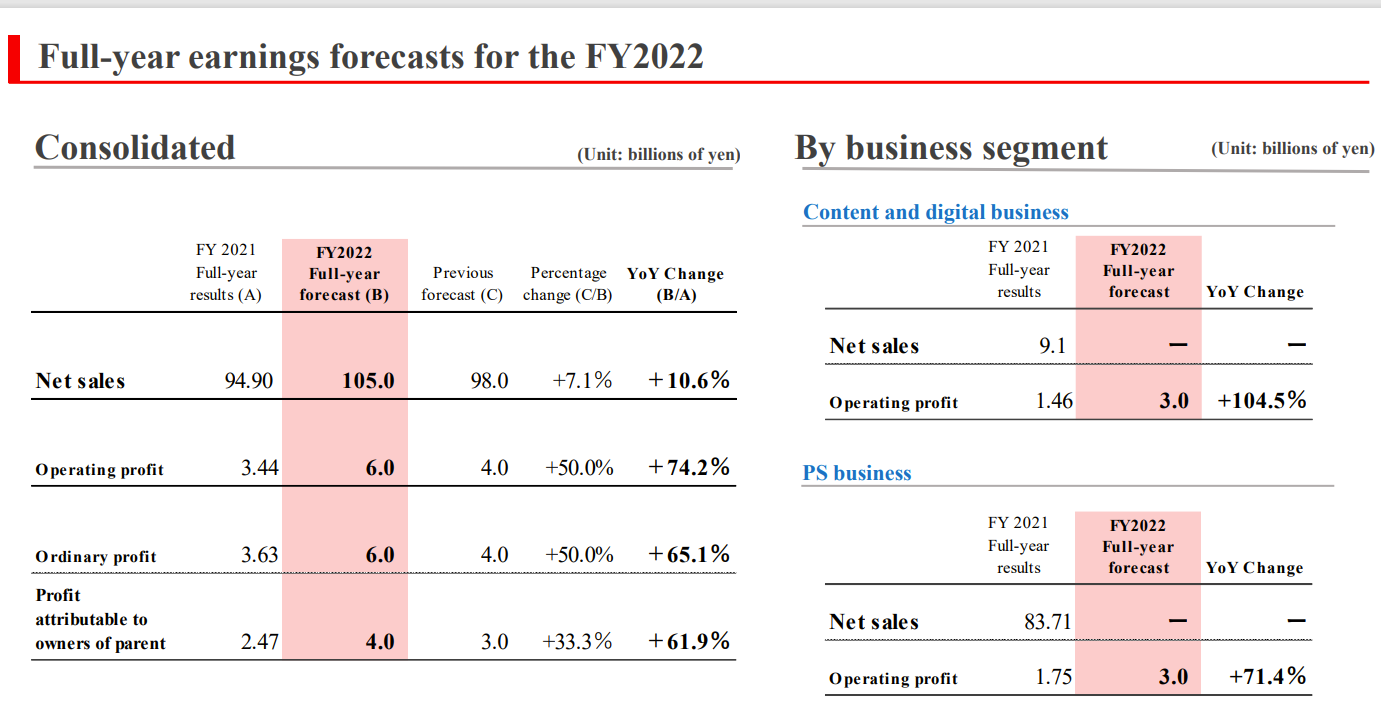

2. Sales and earnings guidance upped for FY 3/23

(Source: Financial presentations for the 2nd quarter of FYE 3/23)

The company increased its sales and profit forecast for FYE 3/23 on 10/24/22 to reflect 1) renewed popularity of flagship content Ultraman and 2) stronger content merchandising and trading card sales especially in China during the first 6 months of FYE 3/23.

3. An independent machine distributor

As a largest independent pachinko machine distributor, it does not belong to a single content company group. Thus, TFH can advise and help pachinko equipment manufacturers develop new product lines which meet the current market AND regulatory requirements. Concurrently, the company aids a client pachinko hall in selecting a machine with promising titles/contents.

4. The 2nd growth leg: Content

Tsuburaya Production’s flagship content Ultraman has regained its popularity, reaching JPY1.4bn in FY03/22 (+94.2% YoY). In Japan, Tsuburaya Imagination digital platform service (started in 2021), and the official Ultraman channel on YouTube (2.24mn subscribers) have led to an increase in sales of toys and other products, contributing to a rise in merchandising and licensing revenue.

Ultraman success was the main reason for upward revision in operating income to JPY 6 bn.

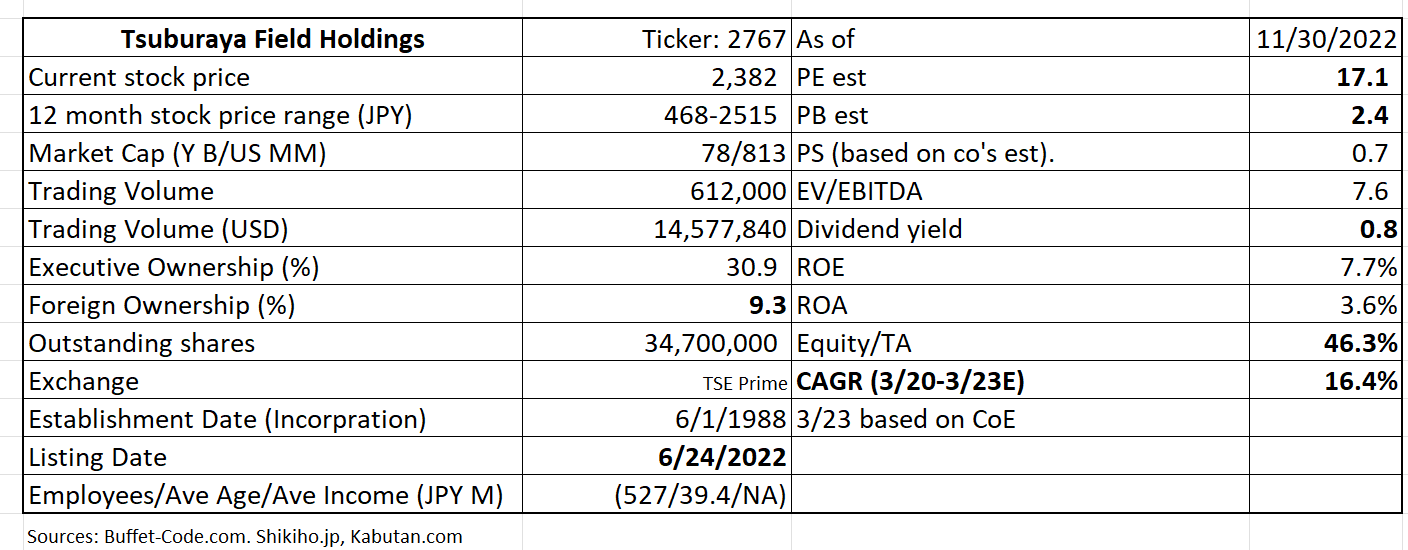

2. Technically Speaking

(Source: buffet-code.com)

The company’s recent profit upward revision has been well received and its shares are trading at a near historical high with a large trading volume.

3. Business Model

1) Content:

Merchandising and licensing revenue is associated with the licensing of intellectual property rights. Tsuburaya Productions earns this revenue by granting the right to use Ultraman and other characters for toys, food products, apparel, publications, and advertisements.

2) Pachinko and Pachislot:

1: The company acquires “merchandising rights” to “promising contents” from Japan and global sources. Contents include anime, manga, and special effects videos.

2: It then adds “value” by combining these contents which will be developed into a product most suitable to a particular pachinko hall. The company is a fabless company, thus, all manufacturing is outsourced. As the largest independent distributor with a nationwide network of 35 offices, the company enables the client pachinko halls to buy titles from various machine manufacturers.

4. Financial Highlights

Financial results for the fist quarter ending 9/22 vs 9/21

Fluctuations in the company’s results are mainly due to the planning, development, and sales of amusement machines in the pachinko and pachislot machines business.

(Source: Financial Highlights for the 2nd quarter for the fiscal year ending 3/31/23)

(Source: Financial Highlights for the 2nd quarter for the fiscal year ending 3/31/23)

The above overall results highlight that net sales as whole rose by 13% y/y with content merchandizing sales was the major driver. Pachinko/Pachislot segments brought in positive profits vs. deficits a year ago period.

Financial Guidance for FYE 3/22

As discussed in Investment Thesis above, TFP increased its financial guidance for FYE 3/22. Notably, operating profit guidance was increased by 50% vs earlier guidance (in red shaded column in table noted Consolidated) thanks to strengths in both content and pachinko/pachislot operations.

(Source: Financial Highlights for the 2nd quarter for the fiscal year ending 3/31/23)

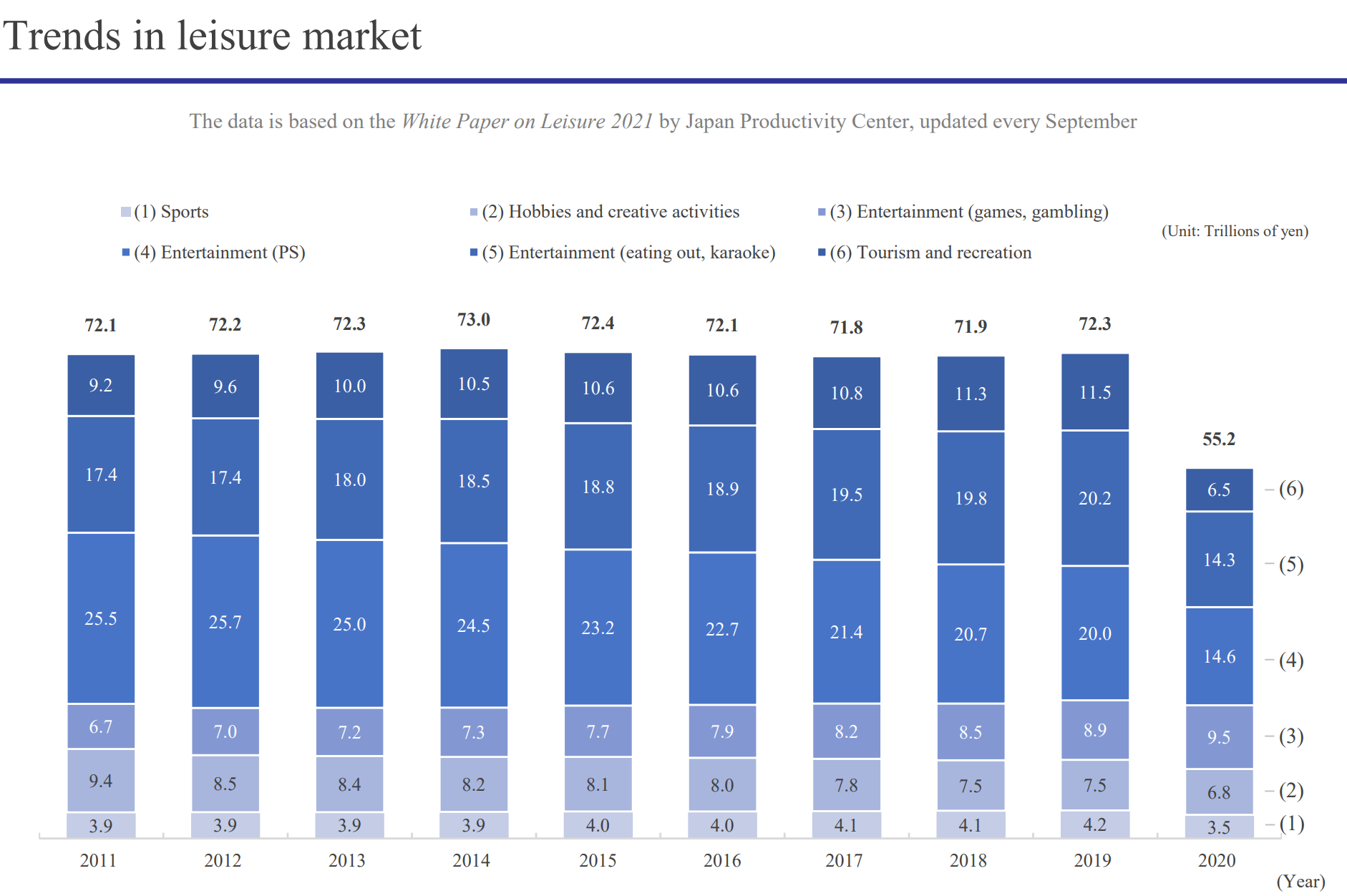

5. Total Addressable Markets (TAM)

TFH competes for consumers’ leisure hours with other entertainment players. As the below bar chart indicates that leisure spending, sports and tourism in particular, decreased in 2021 under the negative Covid impacts. Pachinko and Pachislot spending (denoted as 4, in the below bars) has shrunk even pre-covid due to the aforementioned tighter regulations. However, spending for games and gambling (horse and boat racing, etc), which is denoted 3 in the below bar chart, is rising. TFH believes that it can aim to gain some mind shares of consumers from gaming and even other entertainment segments.

Total pachinko and pachislot machine sales which was on a constant decline since 2006 saw the first uptick in 2021. The one year may not signal a trend reversal, but the trend shift from high gambling to more casual entertainment by the pachinko industry may finally be bearing fruits in bringing back the players.

6. Strengths and Weaknesses

1. The largest independent player

The company is the largest independent distributor with a nationwide network. Through TFH, a client pachinko hall can buy a machine from any manufacturer which is installed with hit gaming contents selected by the company.

2. High entry barrier

The pachinko industry has a high barrier to enter, since 1) there are large and well capitalized incumbents to compete with and 2) large initial investments required. TFH’s large sales force, which is well known for their industry knowledge, has established long term relationships both with clients and machine makers. This client relationship is very hard to replicate by new entrants.

Weaknesses

The company operates in a highly regulated industry whose impacts the company can’t control. However, it seems that the industry has learned to forecast and cope with the tightening regulation.

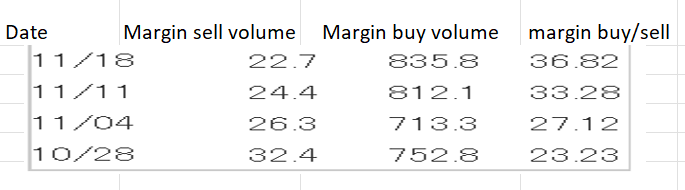

7. Near-term Selling Pressure

As noted in useful tips section of www.JapaneesIPO.com, when the stock’s outstanding margin buy volume is high and rising, that will function as the near-term selling pressure. For Tsuburaya. margin buy sell ratio is high at 37x, but the current outstanding margin buy volume can be easily absorbed in one day trading. Thus, the near term selling pressure is not a big concern.

Margin trading unit (1,000):

(Source: Kabutan.com)

[Disclaimer]

The opinions expressed above should not be constructed as investment advice. This commentary is not tailored to specific investment objectives. Reliance on this information for the purpose of buying the securities to which this information relates may expose a person to significant risk. The information contained in this article is not intended to make any offer, inducement, invitation or commitment to purchase, subscribe to, provide or sell any securities, service or product or to provide any recommendations on which one should rely for financial securities, investment or other advice or to take any decision. Readers are encouraged to seek individual advice from their personal, financial, legal and other advisers before making any investment or financial decisions or purchasing any financial, securities or investment related service or product. Information provided, whether charts or any other statements regarding market, real estate or other financial information, is obtained from sources which we and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future performance